There is very specific language for BYOB in a General Liability Policy. It is called “Host Liquor Liability” or the language found in PICTURE 1 below (see wording in Yellow). The language is found in Exclusion C of the standard GL policy for, which excludes Liquor Liability. However, the “Host Liquor” language is essentially a carve-back where they give you BYOB coverage.

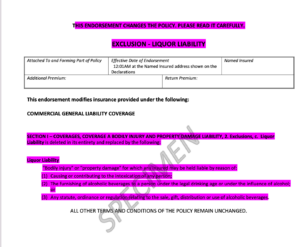

Insurance companies will oftentimes give you “Host Liquor” Language and then will remove it and EXCLUDE BYOB via endorsement (“rider”) via PICTURE 2 below.

Question: if host liquor liability is excluded and a customer gets hurt in the establishment if there is alcohol around does that mean coverage is excluded?

Answer

If host liquor liability is specifically excluded from the insurance policy, it means that any claims arising from injuries caused by a guest’s consumption of alcohol will not be covered by the policy.

However, if a customer gets hurt in the establishment and there is alcohol around, it does not necessarily mean that coverage is automatically excluded. It depends on the circumstances of the incident and whether the injuries were directly caused by the presence of alcohol. For example, if a customer slips and falls on a wet floor near a bar, and alcohol was not a contributing factor to the accident, the insurance coverage may still apply.

It’s important to carefully review the specific terms and exclusions of the insurance policy to understand the extent of coverage provided. If you have questions about your coverage, you should contact your insurance agent or company for clarification.

Picture 1: BYOB or “Host Liquor” Insurance Coverage

Picture 2: The REMOVAL or EXCLUSION of BYOB or “Host Liquor”